Stacey Gauthier at the Renaissance Charter School is worrying a lot these days — about money. This year she’s had to increase class sizes, cut the summer school program, and forgo hiring experienced teachers when an older teacher retires. Yet she still hasn’t cut enough to be able to afford the school’s rising pension costs, which have grown from $12,000 per teacher in 2004 to $21,000 per teacher this year.

Pension costs for city teachers have been rising steadily over the past decade, but for the most part the expenses have been hidden from individual schools, which rely on the city to cover all pension costs. Yet for a small number of charters schools like Renaissance that participate in the Teacher Retirement System (TRS) out of their own budgets, the ballooning price of a comfortable retirement has been acutely felt.

“We have another year to live,” Gauthier said. “We’re dipping into our savings now, which is okay, but if things don’t rebound, we won’t be financially viable.”

Although TRS costs have always been high relative to the private sector, their impact on charter school budgets has become especially burdensome since state lawmakers froze planned increases in charter school funding two years ago. (A breakdown of several charter schools’ pension and 401(k) payments is below the jump.)

The freeze made it harder for schools to pay their TRS contributions, which have increased by 10 percent since 2008. At a loss, schools said their pension payments are often coming at the expense of other school programs — a situation that the district schools could see themselves in if promised budget cuts are approved for next year.

“Our costs are growing astronomically,” said Vicki Zubovic, the managing director of development at the KIPP charter schools. “It’s becoming harder and harder to meet these needs.”

The TRS pension squeeze affects at least 12 charter schools in New York City. The rest offer some sort of 401(k) or 403(b) defined contribution plan in which employees contribute a portion of their salary to a fund and employers agree to match that amount up to a certain percentage.

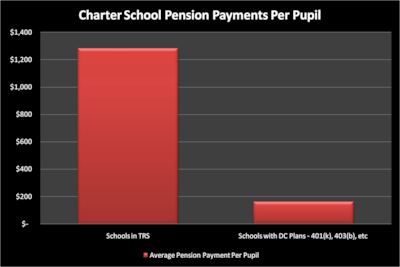

The difference in cost between the two options is enormous.

According to an analysis using the fiscal audits from 2008-2009, on average, non-TRS schools contributed about 2 percent of all payroll expenses to their pension funds. TRS schools contributed around 14 percent of all payroll expenses to the TRS. This comes down to a difference of over $1,400 per student that TRS schools must spend on pensions that other charters are free to direct elsewhere.

Citywide, pensions cost on average $2,000 per pupil — a higher figure than charter schools face because district teachers are generally older and because of the way the TRS accounts for charter school pension costs. Overall, pensions make up $2.1 billion, or 10 percent, of the DOE’s total budget of $21 billion.

Most charter schools in the TRS joined because they are “conversion” schools that transformed into charters from traditional public schools — and as a result were required by the state to keep the same union benefits afforded district school teachers. But a handful of charter schools that belong to TRS opted into the plan on their own.

School leaders said they wanted to offer their employees the same benefits offered by district schools. There is simply no way that a 401(k) plan can offer the benefits that the TRS promises, such as free retiree health care and a guaranteed yearly pension that gets paid whether the market is down or not.

“We knew going in we were going to offer the TRS,” said Leonard Goldberg, the principal of Opportunity Charter School. “It’s hard for a teacher who has five, ten years in a system to try working in a charter school if the charter school doesn’t offer the same benefit.”

Goldberg said that TRS membership has helped Opportunity meet its goal of attracting and retaining experienced teachers. The plan is expensive, he said. But he added, “We believe at the moment it’s worth the investment.”

To compete, some charter schools that don’t participate with TRS have tried to make their 401(k) plans as lucrative as possible.

Take the plan at KIPP S.T.A.R., the only one of the four New York City KIPP schools that is not in the TRS. KIPP S.T.A.R. matches 50 percent of employee contributions up to the federal limit of $16,500 per year. In addition, the school offers employees a partially subsidized health care plan.

Despite all this, KIPP officials conceded that this plan, which is generous by most standards, still can’t compete with the TRS.

Not all unionized charter schools participate in TRS; two that offer 401(k) plans are Amber Charter School in Manhattan and Merrick Academy in Queens.

Even if the TRS schools stop thinking the plan is worth the investment, there’s nothing they can do: According to state law, once a school is in the TRS, it can never leave.

But that hasn’t stopped the schools from asking for relief. Several schools in the plan are pushing to get an increase in state funding to cover the costs. The UFT has proposed pension relief for charter schools that would require the Department Of Education to pay for the schools’ TRS costs. How that would work in practice has yet to be worked out.

But most schools in the plan agree that the simplest option — letting the charter schools opt out of the TRS — would not be a fair resolution.

“I think that there are some ridiculous parts of the pension, but we didn’t set that up,” said Gauthier of Renaissance. “The politicians, traditional public schools, they all have this benefit. Why are charter schools expected to be the sacrificial lambs?”

Here is a breakdown of charter schools’ pension plans and payments, as reported in their 2008-2009 audited financial statements. One note before reading: A small contribution to a school’s pension fund does not necessarily indicate poor policy on the part of the school. Because 401k/403b plans state that an employer must contribute to the plan only if an employee contributes, some schools contribute little to no money to their pension plans due to their employees’ decisions.